As the geopolitical crisis in Ukraine intensifies the Ukrainian auto market could feel the impact as the situation appears to have seriously deteriorated over the past few weeks.

UPDATE: 24 February. The crisis in Ukraine has deepened further with the start of extensive Russian military actions in Ukraine this morning. In terms of risks and further economic sanctions targeted by the West on Russia, as well as automotive sector outcomes, the gloomier scenarios described below now carry more weight.

A build-up of Russian military forces close to the border has led to rising tensions and raised fears of a broader conflict far beyond the ongoing skirmishes between the Ukraines military and pro-Russian rebels in the eastern Ukraines Donbas region. The decision by Russias government to recognise separatist provinces in eastern Ukraine significantly raises the ante as it provides a possible pretext for Russian forces to cross the border into Ukraine under a peacekeeping mission. That in turn would likely provoke more sanctions from Western governments, while also raising the dangers of a broader, longer and more extensive military conflict inside Ukraine. Besides the serious consequences for both countries involved, the crisis is also generating concerns over international economic impacts and associated uncertainties.

Economic impacts will potentially include sharp reversals for the economies of Ukraine and Russia as well as broader indirect effects on the global economy through higher energy prices, for example. Outcomes will ultimately depend on the path and longevity of the geopolitical crisis, but a look at automotive data gives an indication of where immediate risks lay for the sector.

Ukraines vehicle market has been depressed for a while now

According to GlobalData, the Ukrainian economy and light vehicle (LV) market was decimated first by the global financial crisis and then by the economic collapse prompted by the annexation of Crimea by Russia in 2014. From a peak of 664k in 2008, LV demand slumped to 167k in 2009 and following a slow recovery to just over the 200k threshold dropped to a low point of just 50k in 2015. Since then, the recovery has been protracted and painful. An embryonic revival was choked off by the global pandemic in 2020, but in 2021 Ukraine was one of the few countries to achieve strong growth despite the global semiconductor shortage as demand picked up by 23%.

Light vehicle production activity in Ukraine is limited to a handful of SKD (semi-knocked down) kit assembly operations which accounted for just over 7k cars in 2021. In 2008, Ukrainian LV production exceeded 400k but since Ukrainian producer AvtoZAZ stopped building its own brand cars a few years ago most attempts to set up assembly operations have met with failure. Ukrainian assembler Eurocar still builds some koda models for the local market (3.5k in 2021) and AvtoZAZ currently assembles a range of Lada and Kia badged cars purely to get round the ban on the import of built-up Russian vehicles. There have been few indications that Ukraine can hope to attract significant investment in its automotive industry in the near-term.

Russias vehicle market has also been depressed

In contrast, assisted by a population of 146 million, the Russian LV market offers greater potential having reached a peak in 2012 of 2.94 million units although expectations that it was set to become the largest light vehicle market in Europe, overtaking Germany, were not fulfilled. Hit by the fallout from the annexation of Crimea in 2014, sales collapsed in 2015 and continued to fall, reaching a low point of 1.43 million in 2016. Since then, government incentives supported the market to some extent, but lacklustre economic growth and disappointing real income growth have held back progress. COVID-19 brought about further disruption in 2020 as demand dropped below 1.6 million again. In 2021, the demand for personal transportation strengthened against the background of the global pandemic but supply constraints, due to component shortages, mean that the recovery was much weaker than it might otherwise have been. LV sales totalled 1.67 million for the year, +4% compared to 2020 but still almost 1.3 million below Russias historical peak.

The failure to deliver the kind of volume growth it promised 10 years ago, combined with onerous local content requirements and a challenging regulatory framework meant that some global OEMs, who had invested in Russia, decided to cut their losses. GM curtailed its Russian operations from 2015, closing its St Petersburg assembly plant. Ford closed its car assembly plants in 2019, although the Transit is still built in Russia with a local partner. The challenges associated with the development of export sales particularly beyond the immediate CIS markets meant that the failure of the Russian market to achieve growth has been critical. Over 2 million Light Vehicles were built in Russia in 2012 but after the local market-led slump, growth has been elusive and fewer than 1. 5 million LVs came off Russian production lines in 2021.

Renault will watch on a little nervously

Its often little more than a footnote in Renault-Nissan-Mitsubishi Alliance reporting, but Russian domestic giant AvtoVAZ is effectively owned by Renault via a 69%-32% JV with Rostec. Economic sanctions on Russia could impact supplies of parts that are imported including semiconductors from Asia. However, Russias economy has been generally nudged into greater self-sufficiency by sanctions in place since Russias annexation of Crimea in 2014. AvtoVAZ has historically operated at a high level of vertical integration and most parts supplies are domestically sourced. Recent comments reportedly made by AvtoVAZ CEO Nicolaus Maure point to the company making preparations and investigating alternatives in the event of possible supply disruptions. It is not beyond the realms of possibility that a high-level political deal or understanding has been worked out with China as an alternative source for some critical supplies in the event of supply difficulties.

Also of concern to AvtoVAZ will be the sluggish domestic economy and market. Some economists have noted that while sanctions will undoubtedly hurt Russias economy, there is a resilience factor in Russian banks high foreign currency reserves, while rising energy prices offer a lift to Russias huge energy sector.

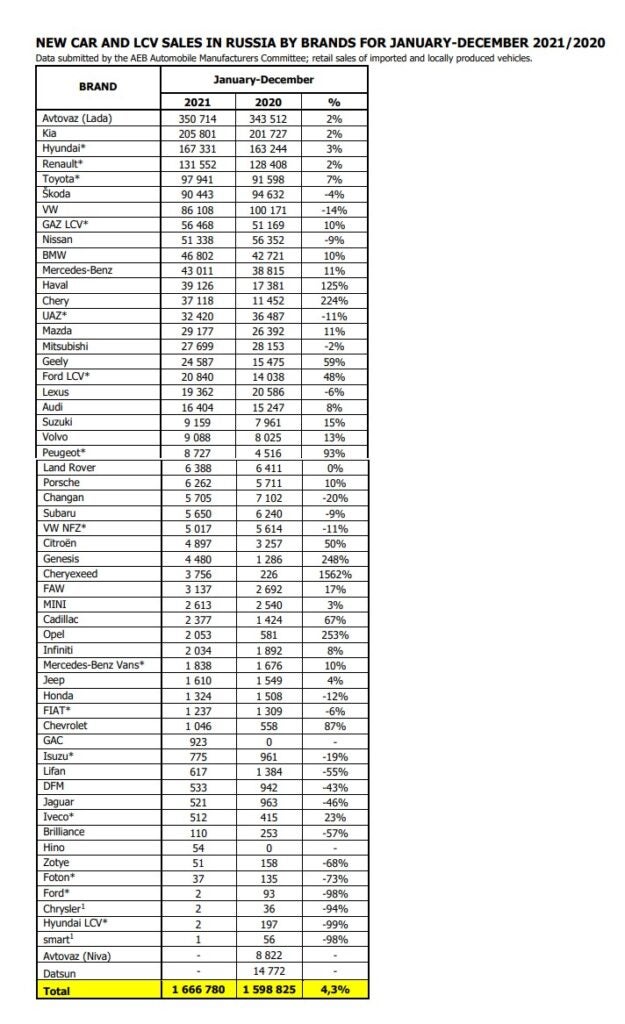

A look at the AEBs LV sales data for full-year 2021 offers an indication of Russia market volume risk by OEM.

Risks

A range of sanctions on Russia from the EU and US have been in place since 2014 and further measures principally affecting the financial, energy and defence sectors were introduced in protest at Russian actions, most latterly following the attack on Alexei Navalny in August 2020. Although they have undoubtedly curtailed economic growth which has averaged an anaemic 1.7% p/a over 2016-2019 it is difficult to disentangle the impact of sanctions from the weaker oil price over the period. It is also the case that Russia has managed to build up some resistance to the threat of further sanctions. Since 2014 it has amassed a significant foreign exchange cushion and now boasts a National Wealth Fund of over $182 bn, close to 12% of GDP. Tensions are bolstering the oil price, which is now over $100 a barrel.

New sanctions from the US and/or the EU could include restrictions on the Nord Stream 2 pipeline (Germany says it will now not be certified), cutting off Russia from the SWIFT international payment system, curbs on big banks, entities, and individuals (including Vladimir Putin). They could also involve a ban on exports of key goods to Russia such as semiconductors, a measure which would undoubtedly impact vehicle production. GAZ Group has been under the threat of sanctions since 2018 but could potentially be denied access to suppliers as the US ramps up the pressure on the Russian LCV producer.

Under the best-case scenario, if the situation is de-escalated and some form of settlement is agreed, the Russian Light Vehicle market could still achieve growth in 2022, albeit at a slower pace than in 2021 when it rose by +4.3% YoY. Risks to this outturn already exist arising from ongoing component shortages and associated production stoppages whilst Russia is dealing with record COVID-19 cases as the omicron variant spreads, although significant restrictions are not currently anticipated. A worst-case scenario sees further pressure on the rouble, prohibitive interest rate rises, significant price hikes, a collapse in consumer confidence and the risk of severe disruption to the supply of components and vehicles to Russia. Sales could drop to 1.1-1.3 mn units, a reduction of up to 35% YoY.

Russian production could also still grow in 2022 if full-scale military conflict is avoided, particularly as export demand has been picking up of late. Just 81k PVs were exported by Russian OEMs in the first 11 months of 2021, but that figure was up 39% YoY. From 2022, export growth should be supported by the decision by Stellantis to start exporting vans from Russia to Europe, Latin America, and Africa. Although expectations are modest for 2022 at less than 10k, at least 40k is targeted for 2023. Such sourcing plans could be vulnerable to change unless tensions improve. However, Stellantis along with most of the other players still present in Russia have been there for some time and have already lived through a succession of crises.

Since the Ukrainian market is still relatively small at 115k in 2015, volume risks are quite limited. A worst-case scenario in the event of a full-scale military incursion from Russian could see demand fall to 40-50k in 2022, a drop of 65-75k units. Renault-Nissan-Mitsubishi, which accounted for 24% of sales in 2021 is the most exposed to this risk, followed by Toyota and Hyundai Groups.

Ukrainian assembly volumes are small (7.3k in 2021) and so the downside risk to output is limited. In the event of a military incursion, supplies of kits, particularly from Russia of Lada badged cars and the Kia Rio would most likely be significantly affected.

Whereas the relatively small Ukrainian market is almost exclusively dominated by imports, principally from the EU and Japan, over 80% of Russian vehicle sales were sourced locally last year. Just 7% of Russian sales were imported from the EU, 3% from Japan and 3% from China.